By F. William Engdahl, author of Myths, Lies and Oil Wars 13 March 2013 Русский перевод: Пузырь сланцевого газа в США лопнул At a time when much of the world is looking with a mix of envy and excitement at the recent boom in USA unconventional gas from shale rock, when countries from China to Poland to France to the UK are beginning to launch their own ventures into unconventional shale gas extraction, hoping it is the cure for their energy woes, the US shale boom is revealing itself to have been a gigantic hyped confidence bubble that is already beginning to deflate. Carpe diem! Part I: America: The New Saudi Arabia? If we’re to believe the current media reports out of Washington and the US oil and gas industry, the United States is about to become the “new Saudi Arabia.” We are told she is suddenly and miraculously on the track to energy self-sufficiency. No longer need the US economy depend on high-risk oil or gas from the politically unstable Middle East or African countries. The Obama White House energy adviser, Heather Zichal, has even shifted her focus from pushing carbon cap ‘n trade schemes to promoting America’s “shale revolution.”i In his January 2012 State of the Union Address to Congress, President Obama claimed that, largely owing to the shale gas revolution, “We have a supply of natural gas that can last America nearly 100 years.” ii Renowned energy experts like Cambridge Energy Research’s Daniel Yergin in recent Congressional testimony waxed almost poetic about the purported benefits of the recent US shale oil and gas exploitation: “The United States is in the midst of the ‘unconventional revolution in oil and gas’ that, it becomes increasingly apparent, goes beyond energy itself.” He didn’t explain what exactly energy going beyond energy itself means. He also claimed that “the industry supports 1.7 million jobs – a considerable accomplishment given the relative newness of the technology. That number could rise to 3 million by 2020.”iii Very impressive numbers. Mr Yergin went on to suggest a major geopolitical dimension of America’s shale oil and gas industry, saying “expansion of US energy exports will add an additional dimension to US influence in the world…Shale gas has risen from two percent of domestic production a decade ago to 37 percent of supply, and prices have dropped dramatically. US oil output, instead of continuing its long decline, has increased dramatically – by about 38 percent since 2008. Just the increase since 2008 is equivalent to the entire output of Nigeria, the seventh-largest producing country in OPEC...People talk about the potential geopolitical impact of the shale gas and tight oil. That impact is already here…”iv In their Energy Outlook to 2030, published in 2012, BP’s CEO Bob Dudley sounded a similar upbeat projection of the role of shale gas and oil in making North America energy independent of the Middle East. BP predicted that growth in shale oil and gas supplies—“along with other fuel sources”—will make the western hemisphere virtually self-sufficient in energy by 2030. In a development with enormous geopolitical implications, a large swath of the world including North and South America would see its dependence on oil imports from potentially volatile countries in the Middle East and elsewhere disappear, BP added.v There’s only one thing wrong with all the predictions of a revitalized United States energy superpower flooding the world with its shale oil and shale gas. It’s based on a bubble, on hype from the usual Wall Street spin doctors. In reality it is becoming increasingly clear that the shale revolution is a short-term flash in the energy pan, a new Ponzi fraud, carefully built with the aid of the same Wall Street banks and their “market analyst” friends, many of whom brought us the 2000 “dot.com” bubble and, more spectacularly, the 2002-2007 US real estate securitization bubble.vi A more careful look at the actual performance of the shale revolution and its true costs is instructive. Part II: Halliburton Loopholes One reason we hear little about the declining fortunes of shale gas and oil is that the boom is so recent, reaching significant proportions only in 2009-2010. Long-term field extraction data for a significant number of shale gas wells only recently is coming to light. Another reason is that there have grown up huge vested corporate interests from Wall Street to the oil industry who are trying everything possible to keep the shale revolution myth alive. Despite all their efforts however, data coming to light, mostly for the review of industry professionals, is alarming. Shale gas has recently come onto the gas market in the US via use of several combined techniques developed among others by Dick Cheney’s old company, Halliburton Inc. Halliburton several years ago combined new methods for drilling in a horizontal direction with injection of chemicals and “fracking,” or hydraulic fracturing of the shale rock formations that often trap volumes of natural gas. Until certain changes in the last few years, shale gas was considered uneconomical. Because of the extraction method, shale gas is dubbed unconventional and is extracted in far different ways from conventional gas. The US Department of Energy’ EIA defines conventional oil and gas as oil and gas “produced by a well drilled into a geologic formation in which the reservoir and fluid characteristics permit the oil and natural gas to readily flow to the wellbore.” Conversely, unconventional hydrocarbon production doesn’t meet these criteria, either because geological formations present a very low level of porosity and permeability, or because the fluids have a density approaching or even exceeding that of water, so that they cannot be produced, transported, and refined by conventional methods. By definition then, unconventional oil and gas are far more costly and difficult to extract than conventional, one reason they only became attractive when oil prices soared above $100 a barrel in early 2008 and more or less remained there. To extract the unconventional shale gas, a hydraulic fracture is formed by pumping a fracturing fluid into the wellbore at sufficient pressure causing the porous shale rock strata to crack. The fracture fluid, whose precise contents are usually company secret and extremely toxic, continues further into the rock, extending the crack. The trick is to then prevent the fracture from closing and ending the supply of gas or oil to the well. Because in a typical fracked well fluid volumes number in millions of gallons of water, water mixed with toxic chemicals, fluid leak-off or loss of fracturing fluid from the fracture channel into the surrounding permeable rock takes place. If not controlled properly, that fluid leak-off can exceed 70% of the injected volume resulting in formation matrix damage, adverse formation fluid interactions, or altered fracture geometry and thereby decreased production efficiency.vii Hydraulic fracturing has recently become the preferred US method of extracting unconventional oil and gas resources. In North America, some estimate that hydraulic fracturing will account for nearly 70% of natural gas development in the future. Why have we just now seen the boom in fracking shale rock to get gas and oil? Thank then-Vice president Dick Cheney and friends. The real reason for the recent explosion of fracking in the United States was passage of legislation in 2005 by the US Congress that exempted the oil industrys hydraulic fracking, astonishing as it sounds, from any regulatory supervision by the US Environmental Protection Agency (EPA) under the Safe Drinking Water Act. The oil and gas industry is the only industry in America that is allowed by EPA to inject known hazardous materials - unchecked - directly into or adjacent to underground drinking water supplies.viii The 2005 law is known as the "Halliburton Loophole." Thats because it was introduced on massive lobbying pressure from the company that produces the lions share of chemical hydraulic fracking fluids - Dick Cheneys old company, Halliburton. When he became Vice President under George W. Bush in early 2001, Cheney immediately got Presidential responsibility for a major Energy Task Force to make a comprehensive national energy strategy. Aside from looking at Iraq oil potentials as documents later revealed, the energy task force used Cheneys considerable political muscle and industry lobbying money to win exemption from the Safe Drinking Water Act. ix During Cheneys term as vice president he moved to make sure the Governments Environmental Protection Agency (EPA) would give a green light to a major expansion of shale gas drilling in the US. In 2004 the EPA issued a study of the environmental effects of fracking. That study has been called "scientifically unsound" by EPA whistleblower Weston Wilson. In March of 2005, EPA Inspector General Nikki Tinsley found enough evidence of potential mishandling of the EPA hydraulic fracturing study to justify a review of Wilsons complaints. The Oil and Gas Accountability Project conducted a review of the EPA study which found that EPA removed information from earlier drafts that suggested unregulated fracturing poses a threat to human health, and that the Agency did not include information that suggests "fracturing fluids may pose a threat to drinking water long after drilling operations are completed."x Under political pressure the report was ignored. Fracking went full-speed ahead.

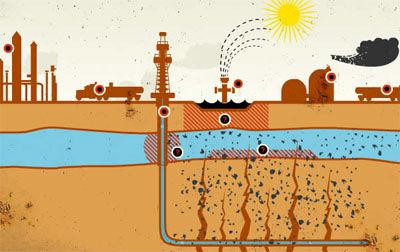

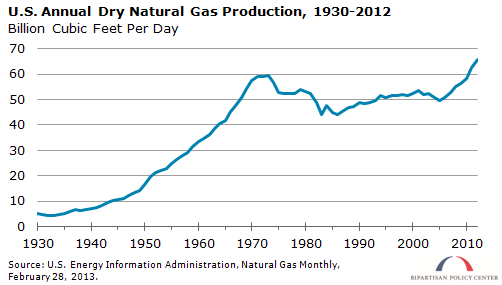

© n/a Fracking toxic waste This diagram depicts methane gas and toxic water contaminating the drinking water as the fracturing cracks penetrate the water table. The Halliburton Loophole is no minor affair. The process of hydraulic fracking to extract gas involves staggering volumes of water and of some of the most toxic chemicals known. Water is essential to shale gas fracking. Hydraulic fracturing uses between 1.2 and 3.5 million US gallons (4.5 and 13 million liters) of water per well, with large projects using up to 5 million US gallons (19 Million liters). Additional water is used when wells are refractured; this may be done several times. An average well requires 3 to 8 million US gallons of water over its lifetime.xi Entire farm regions of Pennsylvania and other states with widespread hydraulic fracking report their well water sources have become so toxic as to make the water undrinkable. In some cases fracked gas seeps into the home via the normal water faucet. During the uproar over the BP Deepwater Horizon Gulf of Mexico oil spill, the Obama Administration and the Energy Department formed an Advisory Commission on Shale Gas, ostensibly to examine the growing charges of environmental hazards from shale gas practices. Their report was released in November 2011. It was what could only be called a "whitewash" of the dangers and benefits of shale gas. The commission was headed by former CIA director John M. Deutch. Deutch himself is not neutral. He sits on the board of the LNG gas company Cheniere Energy. Deutch’s Cheniere Energy’s Sabine Pass project is one of only two current US projects to create an LNG terminal to export US shale gas to foreign markets.xii Deutch is also on the board of Citigroup, one of the worlds most active energy industry banks, tied to the Rockefeller family. He also sits on the board of Schlumberger, which along with Halliburton, is one of the leading companies doing hydraulic fracking. In fact, of the seven panel members, six had ties to the energy industry, including fellow Deutch panel member and shale fracking booster, Daniel Yergin, himself a member of the National Petroleum Council. Little surprise that the Deutch report called shale gas, "the best piece of news about energy in the last 50 years." Deutch added, "Over the long term it has the potential to displace liquid fuels in the United States." xiii Part III: Shale gas -- Racing against the clock With regulatory free-rein, now also backed by the Obama Administration, the US oil and gas industry went full-power into shale gas extraction, taking advantage of high oil and natural gas prices to reap billions in quick gains. According to official US Department of Energy Energy Information Administration data, shale gas extraction ballooned from just under 2 million MCF in 2007, the first year data was tracked, to more than 8,500,000 Mcf by 2011, a fourfold rise to comprise almost 40% of total dry natural gas extraction in the USA that year. In 2002 shale gas was a mere 3% of total gas.xiv

Here enters the paradox of the US “shale gas revolution.” Since the days of oil production wars more than a century ago, various industry initiatives had been created to prevent oil and later gas price collapse due to over-production. During the 1930’s there was discovery of the huge East Texas oilfields, and a collapse of oil prices. The State of Texas, whose Railroad Commission (TRC) had been given regulatory powers not only over railroads but also over oil and gas production in what then was the world’s most important oil producing region, was called in to arbitrate the oil wars. That resulted in daily statewide production quotas so successful that OPEC later modeled itself on the TRC experience. Today, with federal deregulation of the oil and gas industry, such extraction controls are absent as every shale gas producer from BP to Chesapeake Energy, Anadarko Petroleum, Chevron, Encana and others all raced full-tilt to extract the maximum shale gas from their properties. The reason for the full-throttle extraction is telling. Shale Gas, unlike conventional gas, depletes dramatically faster owing to its specific geological location. It diffuses and becomes impossible to extract without the drilling of costly new wells. The result of the rapidly rising volumes of shale gas suddenly on the market was a devastating collapse in the market price of that same gas. In 2005 when Cheney got the EPA exemption that began the shale boom, the marker US gas price measured at Henry Hub in Louisiana, at the intersection of nine interstate pipelines, was some $14 per thousand cubic feet. By February 2011 it had plunged amid a gas glut to $3.88. Currently prices hover around $3.50 per tcf.xv In a sobering report, Arthur Berman, a veteran petroleum geologist specialized in well assessment, using existing well extraction data for major shale gas regions in the US since the boom started, reached sobering conclusions. His findings point to a new Ponzi scheme which well might play out in a colossal gas bust over the next months or at best, the next two or three years. Shale gas is anything but the “energy revolution” that will give US consumers or the world gas for 100 years as President Obama was told. Berman wrote already in 2011, “Facts indicate that most wells are not commercial at current gas prices and require prices at least in the range of $8.00 to $9.00/mcf to break even on full-cycle prices, and $5.00 to $6.00/mcf on point-forward prices. Our price forecasts ($4.00-4.55/mcf average through 2012) are below $8.00/mcf for the next 18 months. It is, therefore, possible that some producers will be unable to maintain present drilling levels from cash flow, joint ventures, asset sales and stock offerings.” xvi Berman continued, “Decline rates indicate that a decrease in drilling by any of the major producers in the shale gas plays would reveal the insecurity of supply. This is especially true in the case of the Haynesville Shale play where initial rates are about three times higher than in the Barnett or Fayetteville. Already, rig rates are dropping in the Haynesville as operators shift emphasis to more liquid-prone objectives that have even lower gas rates. This might create doubt about the paradigm of cheap and abundant shale gas supply and have a cascading effect on confidence and capital availability.” xvii

What Berman and others have also concluded is that the gas industry key players and their Wall Street bankers backing the shale boom have grossly inflated the volumes of recoverable shale gas reserves and hence its expected supply duration. He notes, “Reserves and economics depend on estimated ultimate recoveries (EUR) based on hyperbolic, or increasingly flattening, decline profiles that predict decades of commercial production. With only a few years of production history in most of these plays, this model has not been shown to be correct, and may be overly optimistic….Our analysis of shale gas well decline trends indicates that the Estimated Ultimate Recovery per well is approximately one-half the values commonly presented by operators.” xviii In brief, the gas producers have built the illusion that their unconventional and increasingly costly shale gas will last for decades. Basing his analysis on actual well data from major shale gas regions in the US, Berman concludes however, that the shale gas wells decline in production volumes at an exponential rate and are liable to run out far faster than being hyped to the market. Could this be the reason financially exposed US shale gas producers, loaded with billions of dollars in potential lease properties bought during the peak of prices, have recently been desperately trying to sell off their shale properties to naïve foreign or other investors? Berman concludes: Three decades of natural gas extraction from tight sandstone and coal-bed methane show that profits are marginal in low permeability reservoirs. Shale reservoirs have orders of magnitude lower reservoir permeability than tight sandstone and coal-bed methane. So why do smart analysts blindly accept that commercial results in shale plays should be different? The simple answer is found in high initial production rates. Unfortunately, these high initial rates are made up for by shorter lifespan wells and additional costs associated with well re-stimulation. Those who expect the long-term unit cost of shale gas to be less than that of other unconventional gas resources will be disappointed…the true structural cost of shale gas production is higher than present prices can support ($4.15/mcf average price for the year ending July 30, 2011), and that per-well reserves are about one-half of the volumes claimed by operators. xix Therein lies the explanation for why a sophisticated oil industry in the United States has desperately been producing full-throttle, in a high-stakes game laying the seeds of their own bankruptcy in the process—They are racing to offload the increasingly unprofitable shale assets before the bubble finally bursts. Wall Street financial backers are in on the Ponzi game with billions at stake, much as in the recent real estate securitization fraud. Part IV: 100 Years of Gas? Where then did someone get the number to tell the US President that America had 100 years of gas supply? Here is where lies, damn lies and statistics play a crucial role. The US does not have 100 years of natural gas supply from shale or unconventional sources. That number came from a deliberate blurring by someone of the fundamental difference between what in oil and gas is termed resources and what is called reserves. A gas or oil resource is the totality of the gas or oil originally existing on or within the earth’s crust in naturally occurring accumulations, including discovered and undiscovered, recoverable and unrecoverable. It is the total estimate, irrespective of whether the gas or oil is commercially recoverable. It’s also the least interesting number for extraction. On the other hand “recoverable” oil or gas refers to the estimated volume commercially extractable with a specific technically feasible recovery project, a drilling plan, fracking program and the like. The industry breaks the resources into three categories: reserves, which are discovered and commercially recoverable; contingent resources, which are discovered and potentially recoverable but sub-commercial or non-economic in today’s cost-benefit regime; and prospective resources, which are undiscovered and only potentially recoverable.xx The Potential Gas Committee (PGC), the standard for US gas resource assessments, uses three categories of technically recoverable gas resources, including shale gas: probable, possible and speculative. According to careful examination of the numbers it is clear that the President, his advisers and others have taken the PGC’s latest total of all three categories, or 2,170 trillion cubic feet (Tcf) of gas—probable, possible and purely speculative—and divided by the 2010 annual consumption of 24 Tcf. To get a number between 90 and 100 years of gas. What is conveniently left unsaid is that most of that total resource is in accumulations too small to be produced at any price, inaccessible to drilling, or is too deep to recover economically.xxi Arthur Berman in another analysis points out that if we use more conservative and realistic assumptions such as the PGC does in its detailed assessment, more relevant is the Committee’s probable mean resources value of 550 (Tcf) of gas. In turn, if we estimate, also conservatively and realistically based on experience, that about half of this resource actually becomes a reserve (225 Tcf), then the US has approximately 11.5 years of potential future gas supply at present consumption rates. If we include proved reserves of 273 Tcf, there is an additional 11.5 years of supply for a total of almost 23 years. It is worth noting that proved reserves include proved undeveloped reserves which may or may not be produced depending on economics, so even 23 years of supply is tenuous. If consumption increases, this supply will be exhausted in less than 23 years.xxii There are also widely differing estimates within the US Government over shale gas recoverable resources. The US Department of Energy EIA uses a very generous calculation for shale gas average recovery efficiency of 13% versus other conservative estimates of about half that or 7% in contrast to recovery efficiencies of 75-80% for conventional gas fields. The generously high recovery efficiency values used for EIA calculations allows the EIA to project an estimate of 482 tcf of recoverable gas for the US. In August 2011, the Interior Department’s US Geological Survey (USGS) released a far more sober estimate for the large shale plays in Pennsylvania and New York called Marcellus Shale. The USGS estimated there are about 84 trillion cubic feet of technically-recoverable natural gas under the Marcellus Shale. Previous estimates from the Energy Information Administration put the figures at 410 trillion cubic feet.xxiii Shale gas plays show unusually high field decline rates with very steep trends, a combination giving low recovery efficiencies. xxiv Part V: Huge shale gas losses Given the abnormally rapid well decline rates and low recovery efficiencies, it is little wonder that once the euphoria subsided, shale gas producers found themselves sitting on a financial time-bomb and began selling assets to unwary investors as fast as possible. In a very recent analysis of the actual results of several years of shale gas extraction in the USA as well as the huge and high-cost Canadian Tar Sands oil, David Hughes notes, “Shale gas production has grown explosively to account for nearly 40 percent of US natural gas production. Nevertheless, production has been on a plateau since December 2011; 80 percent of shale gas production comes from five plays, several of which are in decline. The very high decline rates of shale gas wells require continuous inputs of capital—estimated at $42 billion per year to drill more than 7,000 wells—in order to maintain production. In comparison, the value of shale gas produced in 2012 was just $32.5 billion.”xxv He adds, “The best shale plays, like the Haynesville (which is already in decline) are relatively rare, and the number of wells and capital input required to maintain production will increase going forward as the best areas within these plays are depleted. High collateral environmental impacts have been followed by pushback from citizens, resulting in moratoriums in New York State and Maryland and protests in other states. Shale gas production growth has been offset by declines in conventional gas production, resulting in only modest gas production growth overall. Moreover, the basic economic viability of many shale gas plays is questionable in the current gas price environment.”xxvi If these various estimates are anywhere near accurate, the USA has a resource in unconventional shale gas of anywhere between 11 years and 23 years duration and unconventional oil of perhaps a decade before entering steep decline. The recent rhetoric about US “energy independence” at the current technological state is utter nonsense. The drilling boom which resulted in this recent glut of shale gas was in part motivated by “held-by-production” shale lease deals with landowners. In such deals the gas company is required to begin drilling in a lease running typically 3-5 years, or forfeit. In the US landowners such as farmers or ranchers typically hold subsurface mineral rights and can lease them out to oil companies. The gas (or oil) company then is under enormous pressure to book gas reserves on the new leases to support company stock prices on the stock market against which it has borrowed heavily to drill. This “drill or lose it” pressure typically has led companies to seek the juiciest “sweet spots” for fast spectacular gas flows. These are then typically promoted as “typical” of the entire play. However, as Hughes points out, “High productivity shale plays are not ubiquitous, and relatively small sweet spots within plays offer the most potential. Six of thirty shale plays provide 88 percent of production. Individual well decline rates are high, ranging from 79 to 95 percent after 36 months. Although some wells can be extremely productive, they are typically a small percentage of the total and are concentrated in sweet spots.” xxvii

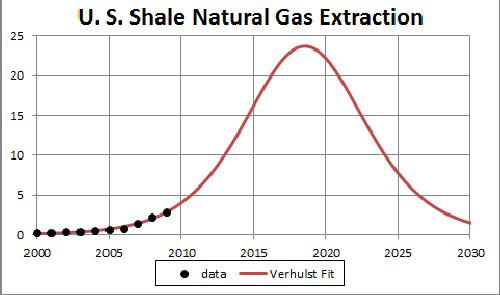

One estimate of projected shale gas decline suggests the peak will pass well before the end of the decade, perhaps in four years, followed with a rapid decline in volume The extremely rapid overall gas field declines require from 30 to 50 percent of production to be replaced annually with more drilling, a classic “tiger chasing its tail around the tree” syndrome. This translates to $42 billion of annual capital investment just to maintain current production. By comparison, all USA shale gas produced in 2012 was worth about $32.5 billion at a gas price of $3.40/mcf (which is higher than actual well head prices for most of 2012). That means about a net $10 billion loss on their shale gambles last year for all US shale gas producers. Even worse, Hughes points out that capital inputs to offset field decline will necessarily increase going forward as the sweet spots within plays are drilled off and drilling moves to lower quality areas. Average well quality (as measured by initial productivity) has fallen nearly 20 percent in the Haynesville, the most productive shale gas play in the US. And it is falling or flat in eight of the top ten plays. Overall well quality is declining for 36 percent of US shale gas production and is flat for 34 percent.xxviii Not surprising in this context, the major shale gas players have been making massive write-downs of their assets to reflect the new reality. Companies began in 2012 reassessing their reserves and, in the face of a gas spot price that was cut in half between July 2011 and July 2012, are being forced to admit that the long-term outlook for natural-gas prices is not positive. The write-downs have a domino effect as bank lending is typically tied to a company’s reserves meaning many companies are being forced to renegotiate credit lines or make distress asset sales to raise cash. Beginning August 2012, many large shale gas producers in the US were forced to announce major write-downs of the value of their shale gas assets. BP announced write-downs of $4.8 billion, including a $1 billion-plus reduction in the value of its American shale gas assets. England’s BG Group made a $1.3 billion write-down of its US shale gas interests, and Encana, a large Canadian shale gas operator made a $1.7 billion write-down on shale assets in the US and Canada, accompanied by a warning that more were likely if gas prices did not recover. xxix The Australian mining giant BHP Billiton is one of the worst hit in the US shale gas bubble as it came in late and big-time. In May, 2012 it announced it was considering taking impairments on the value its US shale-gas assets which it had bought at the peak of the shale gas boom in 2011, when the company paid $4.75 billion to buy shale projects from Chesapeake Energy and acquiring Petrohawk Energy for $15.1 billion.xxx But by far the worst hit is the once-superstar of shale gas, Oklahoma-based Chesapeake Energy. Part VI: Chesapeake Energy: The Next Enron? The company by most accounts that typifies this shale gas boom-bust bubble is the much-hailed leading player in shale, Chesapeake Energy. In August 2012 there were widespread rumors that the company would declare bankruptcy. That would have been embarrassing for the company that was the nation’s second largest gas producer. It would also have signaled to the world the hype that was behind promotion of a “shale energy revolution” from the likes of Yergin and the Wall Street energy promoters looking to earn billions on M&A and other deals in the sector to replace their dismal real estate experiences. In May 2012, Bill Powers of the Powers Energy Investor, wrote of Chesapeake (CHK by its stock symbl): “Over the past year, however, CHK’s business model has broken down. The company’s shares continue to break to 52-week lows and the company has a funding issue—financial speak for the company is running out of money. While it was able to farm-out a portion of its Utica Shale assets in Ohio to France’s Total last year—this is remarkable given the accounting errors that resulted in Total receiving significantly less revenue from their Barnett Shale joint-venture—CHK has largely run out of prospective acreage to farm-out.” Powers estimated a $3 billion cash shortfall in 2012 for the company. That comes atop already huge corporate debt of $11.1 billion of which $1.7 billion was a revolving line of credit. xxxi Powers adds, “When the off-balance sheet debt and preferred issues are added to the company’s existing $11.1 billion of on-balance sheet debt, CHK’s has a whopping $20.5 billion of financial obligations. Given such a high level of indebtedness, CHK debt is rated junk and will be for the foreseeable future. “ He concludes, “Having America’s second largest natural gas producer as well as its most reckless destroyer of shareholder capital almost completely walk away from the shale gas business is a great indication that today’s natural gas price bubble is on the verge of popping. CHK has not made any money by drilling shale wells—and neither have virtually any of its peers—and now the dumb money has run out.” xxxii Angry shareholders forced a major shakeup of the Chesapeake board last September after a Reuters report that CEO Aubrey McClendon had been taking out large loans not fully disclosed to the company’s board or investors. McClendon was forced to resign as Chairman of the company he founded after details leaked out that McClendon has borrowed as much as $1.1 billion in the last three years by pledging his stake in the company’s oil and natural gas wells as collateral.xxxiii In March 2013 the US Government Securities and Exchange Commission (SEC) announced that it was investigating the company and Chief Executive Aubrey McClendon and had issued subpoenas for information and testimony, among other items looking into a controversial program that grants McClendon a share in every well that Chesapeake drills.xxxiv The company is in the midst of a major asset sale of an estimated $6.9 billion to lower debt, including oil and gasfields covering roughly 2.4 million acres. It must invest heavily in drilling new wells to deliver the increased production of more lucrative oil and natural gas liquids, if it is to avoid bankruptcy.xxxv As one critical analyst of Chesapeake put it, “the company’s complex accounting methods make it almost impossible for analysts and stockholders to determine what the risks really are. The fact that the CEO is taking out billion-dollar loans and not openly disclosing them only furthers the perception that everything is not as it appears at Chesapeake – that the company is Enron with drilling rigs.” xxxvi The much-touted shale gas revolution in the USA is collapsing along with the stock shares of Chesapeake and other key players. Endnotes: i Roberta Rampton, Energy Policy Shifting as abundance replaces scarcity: Obama adviser, Reuters, February 25, 2013. v BP, BP Energy Outlook 2030, London, January 2012. vii Glenn S. Penny, et al, Control and Modeling of Fluid Leakoff During Hydraulic Fracturing, Journal of Petroleum Technology, Vol. 37, no. 6, pp. 1071-1081. xi Anthony Andrews, et al, Unconventional Gas Shales: Development, Technology and Policy Issues, Congressional Research Service, Washington D.C., October 30, 2009, p.7. xx SPEE, Canadian Oil and Gas Evaluation Handbook, Volume 1 — Reserves Definitions and Evaluation Practices and Procedures, SECTION 5: DEFINITIONS OF RESOURCES AND RESERVES, Petroleum Society of the Canadian Institute of Mining, Metallurgy and Petroleum, Calgary Chapter, accessed in www.petsoc.org. xxiii Stephen Lacey, After USGS Analysis, EIA Cuts Estimates of Marcellus Shale Gas Reserves by 80% ,August 26, 2011 xxv Arthur E. Berman, After the Gold… xxxvi Jeff Goodell, Op. Cit. |